Going Nuclear

Foreword

We are at an important stage in the development of nuclear energy, with government pledging to deliver Great British Nuclear, a new public body, to bring forward projects and progress existing plans. This is especially timely, as the need for nuclear energy as a vital component of a portfolio of sustainable energy sources is brought into even sharper focus by the energy price crisis.

Recent announcements indicate that policymakers in government agree nuclear energy projects are crucial to reducing our reliance on fossil fuels, support energy security, and help us to meet our net zero ambitions with reliable clean energy. However, there are further policy pathways to take in order to ensure nuclear energy can fulfil its potential, support our transition to net zero and deliver energy security.

This collection features research and evidence-led recommendations from prominent experts in the field of nuclear energy. The University of Manchester’s Dalton Nuclear Institute work closely with the nuclear industry, and highlight the steps needed to develop a policy framework which can secure a long-term nuclear future. From the importance of skills and training, to developing new reactors, to legislative clarity and rapid progression of programmes to meet the 2050 net zero deadline.

Progress in the nuclear industry has followed a pattern of start and stall under successive governments in the last decade – that must change if we are to catalyse our nuclear capability. The Dalton Nuclear Institute and Policy@Manchester recommendations in this collection provide thought leadership on the next steps to secure nuclear energy in a low-carbon and cost-effective energy transition.

Dr Maria Sharmina

Reader in Energy and Sustainability at the Tyndall Centre for Climate Change Research

Policy@Manchester Academic Co-Director

Building nuclear for a greener future

William Bodel, Gregg Butler, Juan Matthews, Francis Livens and Adrian Bull

The UK's ambition to achieve net zero by 2050 is an enormous undertaking, and many acknowledge that achieving such a goal requires an increase in nuclear energy capacity and therefore an increase in the number of nuclear sites across the UK. In this blog, colleagues from the Dalton Nuclear Institute, William Bodel, Adrian Bull, Gregg Butler, Juan Matthews and Francis Livens, assess some of the questions concerning nuclear plant siting which face us.

- The UK is set to miss its next two carbon budgets, the milestones to achieving net zero by 2050.

- This coincides with annual nuclear power output in the UK being at its lowest for 40 years.

- The future vision for nuclear in the UK right now and 2050 is anticipated in three waves, with the final wave of high temperature plants offering potential beyond traditional electricity generation.

- Currently, we do not have enough sites allocated to accommodate an expansion of the nuclear sector of the necessary scale. More sites will be needed, and effort will be needed to gain the local approval needed to proceed with new nuclear build.

The challenge of net zero

In 2019, the UK government legislated to increase its previous ambitions to reduce greenhouse gas (GHG) emissions, committing to net zero emissions by 2050. The Climate Change Act also lays out the carbon budgets – legally binding interim targets for GHG reduction, split into periods of five years. While the first three budgets have been met, the UK is set to miss its fourth and fifth carbon budgets.

Given the challenge of net zero, coupled with the low life cycle of GHG emissions which result from nuclear power, many now acknowledge that expansion of nuclear energy is required if net zero is to be reached. Beyond the environmental motivations, the recent volatility in energy prices has also reiterated the value of a diverse energy mix in protecting energy users from sharp price rises.

Agreement that there is a future for nuclear in the UK is welcome, however time to act is now limited. The UK’s nuclear output has been shrinking since its peak in 1998, owing to the closure of ageing stations – last year’s output was less than half that of 1998, and the lowest since 1982. This lost capacity will have to be replaced before the net output from nuclear energy can increase.

The three wave strategy

To tackle this, the current “Three Wave” strategy envisages the delivery of three broad reactor types over the next thirty years:

- Light Water Reactors (LWRs), such as those currently being constructed at Hinkley Point.

- Small Modular Reactors (SMRs) are small versions of LWRs, anticipated to be deployable in the early 2030s.

- Advanced Modular Reactors (AMRs), assumed to be in the form of High Temperature Gas-cooled Reactors (HTGRs), with ambitions for a demonstrator plant by the early 2030s.

The current generation of LWRs are large and complex engineering projects, with the planned nameplate capacity of Hinkley Point C to be 3.3 GW, for context – the average UK electricity demand during 2018 was 31.4 GW. Building new stations like this takes years, which adds to the overall cost of the electricity produced. By reducing the physical size of LWRs, reactor modules can be built in factories and assembled more easily on-site, reducing costs. More exotic, advanced reactor designs offer potential benefits such as greater uranium efficiency or higher operating temperatures, but are years away from deployment. High temperature reactors are useful because their heat can be used directly in industrial processes which are otherwise difficult to decarbonise, or in generating hydrogen more efficiently than is possible through room temperature electrolysis. Figure 1 shows the imminent decline of the existing reactor fleet, and the potential rebuilding with the Three Waves:

![Graph showing the decline of the existing UK nuclear fleet, and the potential future Three Waves of nuclear [adapted from NIRAB]. The LWR plot assumes successful completion of Hinkley Point C and two sister stations. The graph shows that with future AMRs, SMRs and LWRs, the nuclear capacity could increase dramatically by 2050.](./assets/uw89gntXQ5/nuclear-300x196-300x196.png)

Figure 1. The decline of the existing UK nuclear fleet, and the potential future Three Waves of nuclear [adapted from NIRAB]. The LWR plot assumes successful completion of Hinkley Point C and two sister stations.

Figure 1. The decline of the existing UK nuclear fleet, and the potential future Three Waves of nuclear [adapted from NIRAB]. The LWR plot assumes successful completion of Hinkley Point C and two sister stations.

Ambitious scenarios use examples involving hundreds of reactors to provide the energy needed to replace fossil fuels, less ambitious programmes would still require many tens of reactors on tens of sites. As only eight sites have been deemed potentially suitable for the deployment of new nuclear power stations in England and Wales before the end of 2025, an unavoidable consequence of such a desired expansion of the nuclear sector is a requirement for new sites to host future nuclear plants. This is important, because new sites, i.e. those with no historic nuclear presence, will require the acceptance of new reactor build in areas with surrounding publics with no experience of, or vested interest in, a new local reactor.

Community support for nuclear

When considering new sites for nuclear stations, it is worth bearing in mind that the last UK nuclear site to be opened was Torness, where work on the site’s nuclear plant started over 40 years ago. Both the UK nuclear industry and the processes involved in granting permission to developments have changed very significantly since then – local acceptance looms considerably larger in the process than it did in the past. The necessity for new sites prompts a need for local acceptance of a sort that has not been sought for almost half a century. Assuming community support for new build, even in existing nuclear communities, could prove complacent – especially where previous plants may have been perceived to have damaged the environment or left other negative legacy behind. Important questions will be asked about many aspects of the nuclear legacy, from the traditional concerns around nuclear waste, to that of the decommissioned plants which seem to have become permanent features on the landscape.

The solution

One area where lessons for a potential solution can be found is that of efforts made to find a suitable site to host a nuclear Geological Disposal Facility (GDF). The process has been a long one, with failures resulting from opposition from county council levels in 1997 and 2013, the latter in spite of approval from the district level. The current local consent-based approach seems to be making measured progress on a GDF, with three areas currently involved in local engagement processes. This progress, while modest, might be instructive on how to progress with regional consent for new nuclear energy sites.

The Dalton Nuclear Institute has released a position paper, containing nine recommendations for government and industry. The overarching recommendation is for government to develop an integrated framework for the delivery of nuclear energy in the UK. A solid understanding of the full lifecycle of future nuclear provision will be essential to ensure that a suitable nuclear sector can be delivered by 2050.

William Bodel is a Postdoctoral Research Associate at The University of Manchester’s Dalton Nuclear Institute. His previous work concerned life-extension of operating British reactors, and he is currently engaged in future reactor system choice.

Gregg Butler is Head of Strategic Assessment for The University of Manchester’s Dalton Nuclear Institute. He has published extensively on a broad range of nuclear topics, and was a member of the Committee on Radioactive Waste Management from 2012 to 2019.

Juan Matthews is Visiting Professor in Nuclear Energy Technology at The University of Manchester’s Dalton Nuclear Institute. With a career spanning over 50 years, he has experience in nuclear and high technology industries across Europe, Asia, Russia and the Americas, and was formerly the nuclear specialist at UK Trade and Investment (now Department of International Trade).

Francis Livens is Professor of Radiochemistry. He has acted as an advisor to the nuclear industry both in the UK and overseas and holds a range of external roles, including Chair of the Nuclear Innovation and Research Advisory Board (NIRAB) and a member of the Nuclear Decommissioning Authority Board.

Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

A nuclear society: rebuilding perceptions of nuclear energy

Adrian Bull

The nuclear industry has historically had a fairly tumultuous relationship with wider society. Early perceptions of nuclear energy were generally positive, with it viewed as a beacon of how technology went hand in hand with increasing prosperity. However, a history of highly-publicised leaks, discharges and assorted incidents have created a legacy of societal mistrust of nuclear energy. In this article, Professor Adrian Bull examines what measures can be taken by industry and government to re-invigorate the UK’s nuclear sector and its relationship with the public.

- Nuclear sector communication with the public has lacked engagement and openness – fuelling concerns that the industry has much to hide and little to be proud of.

- Public protests have often been followed by Government capitulation, exacerbated by the long timeframes (spanning multiple elections) which characterise the development and operation of nuclear facilities.

- As government looks to find a site for a Geological Disposal Facility (GDF) for radioactive waste in the UK, the nuclear sector and government should openly engage with much more focus on the potential host communities.

Past incidents of management and safety failures sit alongside other legitimate concerns people hold about radiation and nuclear. These include the silence and invisibility of radiation; the lack of control people feel over any nuclear risk; the fact that when things go wrong, they have the potential to go very badly wrong; the intergenerational legacy of nuclear waste and the fact that nuclear security is often perceived as secrecy. Together all this has made the relationship with society increasingly uncomfortable for the UK nuclear sector. Regrettably, it didn’t always respond well. In many cases, it barely responded at all. The approach used for making nuclear safety cases was applied to communications too. Endless time debating and amending, with multiple additions along the way, then repeated levels of senior level signoff before any statement would finally appear – inevitably long after the conversation had moved on. Often any industry statements were predicated on education of readers into reassurance.

Consequentially, there has been long-standing reluctance from some (often vociferous) parts of society to endorse and support the activities of an industry it sees as intruding malevolently into its communities, rather than adding value.

Communications from government and industry clearly need to change in future, but there are perhaps some encouraging signs. Not always driven by a greater support for the nuclear industry, but more by the changing priorities and values of society itself. We can all see the impact of climate change, which heightens society’s desire to avert more damage (or at least to avoid making things worse with more fossil fuel use). Enhanced concerns over energy security have made people value the baseload power we get from stations that produce electricity 24/7, irrespective of the weather. And the consequences of COVID include greater familiarity with the role of science in public policy and greater willingness among the public to challenge those links and dig further behind the data.

Government should ensure that policy making in relation to energy and climate change is evidence-based, open and transparent, and that the science and data behind policy decisions are published along with the decisions themselves. Essentially a “show your working” approach.

In step with the current Energy Awareness campaign, national and devolved UK governments should support local authorities to invite local communities to discuss how they can contribute towards the UK’s Net Zero commitment, including by hosting low carbon infrastructure of all types, and how they might be rewarded for doing so. Local authorities could lead on this to shape and guide place-based responses.

In lockstep with government, the nuclear sector needs to up its game in the future, too. Not just for proposed new power stations, such as the new generation of Small Modular Reactors – which have the potential to be located within communities with no previous experience of nuclear energy – but also for nuclear waste disposal.

For the first time ever, the approval for a key piece of UK infrastructure will sit with society, rather than with Government. The proposed final resting place for the UK’s higher level nuclear waste – a deep underground disposal site, known as the Geological Disposal Facility (GDF) – will only proceed if the community where it is to be hosted explicitly decide that they want to have it. There is a package of community and financial benefit attached too, but it will be a far-reaching decision for a group of 21st century citizens to make an irrevocable choice to host a huge part of Britain’s nuclear waste inventory below their community for all eternity.

There are currently four communities engaged in the process to select a final GDF location and any decision on a final site is well over a decade away. But if the communities are to remain engaged, the industry needs to think and act differently. Instead of the nuclear sector focusing on a conversation about itself (the nature of the waste and packaging, and the design of the planned repository) conversations should start with a focus on the community. What do they consider to be important? What are their values? How do they even come to identify themselves as a “community” in the first place? How do they want to be viewed by their descendants, many generations into the future?

Government can support this approach by encouraging Nuclear Waste Services to frame conversations with potential GDF host communities around the needs and values of the community itself rather than around nuclear waste and repository design.

If Government and industry can rise to the challenge and start listening before speaking, then there is a real chance of turning nuclear’s relationship with wider society into a much more positive one, for all concerned.

Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

The Energy Security Strategy: Going nuclear

Francis Livens

In April, the government announced plans to build eight new nuclear reactors in the UK, alongside strategies to boost wind, hydrogen, and solar production. These reactors are intended to improve the UK’s energy self-sufficiency and reduce greenhouse gas emissions, as well as creating thousands of new jobs. In this blog, Professor Francis Livens of the Dalton Nuclear Institute breaks down what these plans mean, and the best routes to meeting them.

- If all of the goals in the new strategy are met, nuclear could provide 20 – 25% of our electricity needs by 2050.

- However, this requires rapid action on the part of policymakers, expediting planning approval and minimising our dependence on global supply chains.

- In parallel, the same urgency has to be given to developing new reactors which will meet our low-carbon energy needs beyond the end of the decade.

Having seen the shape of government’s energy security plans, it’s clear they require a fundamental change in the way we ‘do nuclear’. We aren’t going to accelerate from one reactor a decade to one a year, and then onwards to 24 GW (about 15 Hinkley Point C reactors) by 2050, without transforming the whole sector. It’s worth unpicking some of what this plan means.

What are we going to build?

At the moment, the only stations planned or under construction in the UK are EdF’s European Pressurised Water Reactors (EPR), at Hinkley and potentially Sizewell, with two reactors at each site. This is a mature design so deployment will be limited by the supply chain – you order specialist nuclear components many years in advance – and workforce availability. Realistically, if we started today, we’d be doing incredibly well to get Sizewell C operating by the end of the decade, so EdF aren’t going to get us beyond half way to our eight reactors.

If we look elsewhere, there is interest from an American consortium in building two Westinghouse AP1000 reactors at Wylfa on Anglesey. This reactor has already been approved by the UK regulators but has a mixed history, with four operating in China, while some American projects are going badly wrong. The design is workable; the challenge is delivering the project.

Finally, there are ‘Small Modular Reactors’ (SMR). These are quite different in conception, with the aim being to build them in kit form in a factory and then assemble them on site. One contender is the Rolls-Royce SMR. Nobody’s built one of these so far, but it is based on well-understood technology (so not too risky), and the design started the regulatory approval process earlier this month. Approval could take up to four years, and construction of the first reactors a further four or five years, so there’s no slack here if we’re to meet the end-of-decade goal. What’s more, a lot depends on how much risk Rolls-Royce might be prepared to take; for example, building factories and manufacturing components in advance of regulatory approval. With a fair wind, we could have a couple of these by 2030.

The biggest risk on the 2030 timescale is therefore not really the technology, but our ability actually to deliver these big, complex projects – a problem that’s not unique to nuclear or the UK, as we see from the American AP1000 projects, London 2012, or HS2. Setting realistic budgets and schedules will be crucial to ensuring this project is delivered in time to meet the goals laid out in the strategy.

What else do we need?

Nuclear energy isn’t just about the reactor. You need a site to build on and, while it’s likely that all the pre-2030 reactors would use existing nuclear sites, it might be necessary to smooth the transfer of land from the current owner (probably the Nuclear Decommissioning Authority) to the new build developer. There are also several other strands of planning and similar activity which would need to be expedited.

Regulatory approval, which is often seen as a blockage, doesn’t have much impact on the programme before 2030. The EPR and AP1000 have already been approved, though acceleration could take a year or so of the SMR timeline. It might have more impact if other designs came into the frame, but those are more likely beyond 2030, or if we want to introduce advanced technologies, such as the use of digital simulations in design.

The biggest risk is around project delivery. The UK has a nuclear supply chain and a skilled nuclear workforce, but these are spread across decommissioning, new nuclear, and defence, all of which present increasing demand. We are also dependent on global supply chains for some critical elements, and as a result will be in competition with other countries which are following similar thought processes to us. There is no point in having everything ready to go, and then finding yourself waiting 3 years for the reactor pressure vessel.

You can mitigate the supply chain and skills risks by giving the sector confidence to invest, but that requires clarity and commitment from government, and – perhaps hardest of all – a seamless approach across multiple government departments. The new strategy provides a solid framework; the challenge is in ensuring its goals are met on time and at cost, and will require a clear and consistent vision from policymakers.

If we do all this, though, we could just about get to 2050 with nuclear providing 20-25% of our electricity, more or less its historical contribution, and compensating for the loss of the ageing fleet of current reactors between now and 2030.

Beyond 2030?

Even if we act urgently up to 2030 and achieve everything in these energy security plans, we will not have solved our energy problems. Energy is not just electricity (about 40% of UK energy use is electricity; the other 60% is largely fossil fuels) and we have a legally binding commitment to Net Zero by 2050, so we have to keep our eyes on that longer term goal. Nuclear has a potential role here too, since High Temperature Gas-cooled Reactors (HTGR) can provide the heat needed to, for example, decarbonise energy intensive processes such as steel making. This was recognised in the 2020 Energy White Paper, but HTGRs are much less mature and, if we don’t push on with them in parallel with the immediate activities, they won’t be ready when we need them.

The IPCC has made it clear that the time is now to act on climate change. While new nuclear won’t come online in time to ensure greenhouse gas emissions peak in the next three years, rapid progress in the sector today will ensure we lock in a low-carbon future for the decades ahead.

Francis Livens is Professor of Radiochemistry. He has acted as an advisor to the nuclear industry both in the UK and overseas and holds a range of external roles, including Chair of the Nuclear Innovation and Research Advisory Board (NIRAB) and a member of the Nuclear Decommissioning Authority Board.

Location, location, location: finding sites for nuclear power plants

Adrian Bull

Expanding nuclear power should be a key priority as the government aims to cut its carbon emissions. However, finding suitable sites to accommodate the proposed plants raises new questions. In this article, based on the Dalton Nuclear Institute’s position paper, Siting implications of nuclear energy, Professor Adrian Bull gives his view on how policymakers can address these issues.

- Existing plans for new nuclear have concentrated on existing sites, but with the UK running out of suitable land close to these existing reactor sites, consideration must be given to new locations.

- Strict conditions on issues such as environmental protection, safety and emergency planning must be met in new nuclear locations.

- The solution to a clean, ethically sound nuclear future could lie with the government as well as a workforce of nuclear skilled individuals.

We are increasingly seeing encouraging words from leading politicians and their advisors about the need for a series of new nuclear power stations in the UK to help reduce our over-dependence on gas, cut CO2 emissions and maintain energy prices at an affordable level for homes, businesses and public services. But among the questions around such a proposal, one which rarely gets much attention is “Where will they actually go?”.

Historically the nuclear power plants we’ve constructed have both been physically large and have produced a lot of electricity. That’s meant a need to locate them close to a reliable source of cooling water to help remove the excess heat that’s left over after vast quantities of steam pass through the turbines. In the UK, coastal sites are perfect for that, usually removing the need for cooling towers. That approach also fitted with the desire to locate the early plants away from large centres of population, both to avoid widespread public concerns and also as a “just in case” measure in the event of any accidents or the need to evacuate local communities.

We ended the AGR (advanced gas-cooled reactor) programme in the 1980s with around a dozen sites in use – either for the older Magnox stations or the newer AGRs. Sometimes both alongside each other. Almost all these were coastal sites – just Trawsfynydd in North Wales (home to a single Magnox reactor alongside a lake) and Chapelcross in Dumfriesshire (where cooling towers and a pipeline to the nearby coast were used to provide cooling) were inland.

Crucially, no new sites have been added to the list since that time. All plans for new nuclear focus on existing nuclear sites such as Hinkley Point in Somerset (where new reactors are under construction) and Sizewell in Suffolk (home to our newest operating reactor – Sizewell B – and proposed to host a replica of the Hinkley Point development, to be known as Sizewell C).

But where will they actually go?

As government now look to expand the UK’s nuclear fleet once again, we need to think about siting. A nuclear reactor can’t just go anywhere – there needs to be a nuclear site licence which will only be granted to a new site if the right conditions on environmental protection, safety, emergency planning, and so on can be met. Some access to cooling water will be needed. There needs to be a connection to the grid to export the power. And the support (or at least acceptance) of the community and their representatives is also important.

The UK is running out of suitable land close to the existing reactor sites, and large swathes of the existing sites are occupied either with operating reactors or – increasingly – those which have closed down and which are in various stages of decommissioning, scheduled to take a minimum of several decades to complete. It’s worth remembering that the last time that we in the UK built a nuclear power station at a site which hadn’t previously had one was the Torness plant in Scotland – where construction began in 1980!

The development of – and enthusiasm for – small modular reactors (SMRs) is a further factor in the discussion. These are widely expected to play a major part in the new nuclear era for the UK, and a key benefit is that they don’t require the same cooling as traditional bigger plants. So, together with the fact that existing sites can’t support all the new nuclear we need, that implies we’ll see a lot of new locations proposed to host nuclear plants who have little or no experience with nuclear. Some of these could be much closer to big end users of electricity too – such as industrial areas and major cities.

A holistic approach: the nuclear site cycle

The answer to this conundrum perhaps lies – as so often – with Government. Through the Nuclear Decommissioning Authority (NDA) they own most of the decommissioning sites in the UK. Currently their clean-up mission takes no account of the need for Britain to build substantial new nuclear capability. A recommended change would be to employ a holistic approach to the management of sites in the same way that we think of a “nuclear fuel cycle” for the reuse and optimisation of the materials in the nuclear cycle.

A “nuclear site cycle” approach is needed to balance opposing drivers. One driver is the current mission to clean up a site for potential delicensing (which stipulates a very high level of decommissioning – ensuring doses to the public are extremely low – and often unlikely to occur in practice). But that needs to be weighed against the potential value that site could play in a new nuclear build programme. As well as a nuclear site licence, decommissioning sites all have access to cooling water, the potential to reuse or restore appropriate grid connections and local communities which have knowledge and experience in nuclear energy.

Skills, clean-up and community

Perhaps most importantly, the sites must be accompanied by a workforce of nuclear-skilled individuals who would be well placed to support the construction, commissioning and operation of new plants once the existing site decommissioning draws to a close. Helping to re-skill these workers and retain their expertise in the communities which they call home is a vital enabler to support one of the NDA’s socio-economic objectives. Namely to support the maintenance of sustainable local economies for communities living near NDA sites and, where possible, contribute to regional economic growth.

Accelerated or scaled back clean-up of sites to a point where they can safely and cost-effectively be re-used to support a further round of clean, reliable nuclear power generation should urgently be made a part of the NDA’s mission. This needs to happen in parallel with the opening of discussions with potential host communities in areas without nuclear facilities – as I’ve recommended elsewhere.

It would be a cruel irony if – after decades of inaction – we decided as a nation that we wanted much more nuclear, only to find that we had nowhere suitable to put it!

Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

The skills gap for long term nuclear future

Aneeqa Khan

The world’s climate and energy crises continues to worsen with extreme weather, heatwaves and increasing global energy prices. The IEA’s net zero by 2050 pathway has identified the need for nuclear, including SMRs growing support for this in the UK, Canada, France and the US. In this blog, Aneeqa Khan discusses the steps needed to develop a framework to secure a long-term nuclear future.

- The UK should invest in multi-level training opportunities for individuals through apprenticeships, undergraduate and doctoral training, as well as cross industry training for people to move into the new nuclear sector, with a focus on fission (including small modular reactors – SMRs) and fusion.

- Provision of a framework for these opportunities should be made available internationally with a focus on developing countries, and those most vulnerable to climate change.

- The UK nuclear industry should develop strong collaborative partnerships with countries with a developing nuclear industry and foster a culture of knowledge exchange.

Long term energy planning versus short term solutions

In August, EDF shut down the two reactors at Hinkley Point B, equivalent to a loss of almost a GW of power generation. They also said they will extend the use of the West Burton A coal power plant, with discussions continuing to potentially keep a further 2 coal power plants open. Billed as ‘short term’ strategies, these interventions do not provide a long term solution, and contradict the aims of the UK Government’s Energy Security Strategy released in April 2022, which aims to deliver clean energy and commits to building one nuclear reactor a year.

We should be extending existing nuclear technologies to cover the bridging over to advanced nuclear reactors, which must continue to receive funding and support. Issues of finance, regulation, the role of Government, siting, public and community acceptance, as well as the integration of nuclear into wider energy strategies including heat and hydrogen must also be addressed. The energy security strategy needs to address training by working with universities and other education providers to ensure there is no skills shortages across these vital areas.

Investing in education and skills

COP26 and COP27 have recently highlighted the need for more young people to be trained to deliver nuclear energy goals. Government investment in nuclear education and training is needed with a key focus on advanced fission (including SMRs) and fusion reactor concepts.

This should include dedicated modules for undergraduate and postgraduate degrees across a range of disciplines; from science, to engineering and regulation, doctoral training centres that address the challenges in delivering advanced reactor concepts, as well as apprenticeships, and training opportunities in advanced reactor concepts for those already working in a relevant field. The University of Manchester offers a fully funded, four-year Centre for Doctoral Training (CDT) PhD in GREEN (Growing skills for Reliable Economic Energy from Nuclear) in addition to the PhD Fusion Energy CDT.

A lack of adequate investment in skills and training could lead to a shortage in the skilled workforce, which the nuclear industry will need to combat the climate emergency, as part of a sustainable energy mix that includes renewables.

Global collaboration

Climate change adversely affects countries and communities that have least contributed to it. Therefore shared knowledge skills may help to catalyse our global transition towards a low-carbon society. This may allow communities most affected by climate change to benefit from the use of new nuclear energy technology.

Policymakers and the nuclear industry need to work with communities directly in an open and transparent way and work with other industries such as housing, water, solar, and wind in order to find synergies and ways we can share mutual knowledge aiming to combat climate change. According to the World Nuclear Association, there are around 30 countries who are ‘considering, planning or starting nuclear power programmes.’ This includes Bangladesh (where it is predicted up to 1 in 7 people could be displaced by climate change by 2050) where construction of power plants have started, as well as countries with developing plans such as Nigeria, Kenya and Laos.

There are challenges in terms of the grid system – if we talk about large power plants it can be difficult to have large amounts of power in one place for an infrastructure not built for that. If the power plant needs to be taken offline for maintenance, this can be detrimental if it accounts for a significant amount of the electricity on the grid. AMRs (advanced modular reactors) and SMRs may be an answer for this as they will be much smaller. Grid infrastructure may require upgrading in general. Other challenges are the licensing of reactor designs, and often countries with developing nuclear rely on countries with developed nuclear power. Sharing skills will allow countries to have autonomy and support in developing nuclear power and therefore transitioning towards secure, clean energy.

There should also be a focus on countries with existing nuclear power, such as South Africa, Pakistan, and Mexico to further expand and collaborate. This will amplify the UKs position as a global leader on climate responsibility and also foster knowledge exchange of technologies, manufacturing and collaboration.

Only with a collaborative approach that crosses man made borders and incorporates multiple industries will we be able to address the skills gap – creating a future where nuclear plays a role in providing low carbon energy.

Dr Aneeqa Khan is a research fellow in Nuclear Fusion working at the University of Manchester at Harwell and in the School of MACE.

Nuclear power - the role of government

Adrian Bull and William Bodel

In 2006, Prime Minister Tony Blair assured Britain that nuclear was “back on the agenda with a vengeance”. This year the Government has pledged to deliver nuclear at “warp speed”, with all recent Prime Ministers emphasising their support for nuclear. Yet Britain’s first new nuclear plant – Hinkley Point C (HPC) – is still some years from operation and, despite recent progress at Sizewell C, there is no confirmed successor project. In this blog, Adrian Bull and Will Bodel examine the gap between intention and reality and highlight policy recommendations from a new paper by the Dalton Nuclear Policy Group.

- Government should be clear on what it expects for future reactors, particularly concerning size and output.

- Government should make clear long-term decisions, that are consistent, to provide certainty to the market.

- Nuclear programmes must move fast enough to meet the 2050 net zero deadline, and government processes must keep up. This will be particularly crucial to enable an ‘early 2030s’ date for the operation of a demonstration High Temperature Gas Reactor (HTGR) to be met.

Government needs to lead if nuclear is to play its part in hitting Net Zero.

But cost is an issue – conventional reactors like Hinkley Point (HPC) are so expensive that even state-backed EDF didn’t have deep enough pockets to invest without bringing in Chinese partners to take a 1/3 stake. The countries who delivered extensive and rapid rollout of nuclear have all had energy markets which were state-run, and regard the supply of safe, secure electricity as a strategic imperative rather than leaving it to a fickle and uncertain market.

Government’s desire to let markets deliver – but then intervene or backtrack – reduces confidence for investors and the supply chain. Some well-intentioned interventions include:

- The contracts for difference model (used to finance HPC). This was followed by an eventual U-turn on Chinese participation beyond HPC and then adoption of the Regulated Asset Base (RAB) financing model.

- A high-profile competition launched in 2016 by the Department of Energy and Climate Change for the best future small modular reactor (SMR) designs, as part of a £250m investment in an ambitious nuclear research and development programme. This was subsequently downgraded to a consultation, then in February 2022 reissued as an Advanced Modular Reactor (AMR) research, development and demonstration competition.

Free and open competition works well – but takes time and can’t really solve the intertwined crises we currently face of medium-term energy security and longer-term climate preservation. Sometimes a “command and control” approach, putting speed ahead of perfect outcomes, is needed – such as government’s response to the pandemic.

Other factors include very long timescales for delivery of new plants – meaning longer before investors see returns on their money; planning delays; and public opposition if not well handled. Positions on nuclear and its priority for government oscillate, both with changes in leadership and with the other demands facing Whitehall. Brexit, COVID and the current war in Ukraine have, understandably, soaked up precious resources over recent years. All leading to a shaky perception among investors and developers of political commitment and the associated risk.

Perhaps the greatest challenge though is that different aspects of government’s complex role in nuclear sit across Whitehall and are addressed separately. Delivery of new GW-scale nuclear falls under BEIS, whilst longer term innovation on new reactors such as SMRs and AMRs and links with heat and hydrogen supply are elsewhere in BEIS. Then developing the supply chain and value to UK businesses are in yet another area of BEIS. Regulation comes under Work and Pensions. Siting – many prospective sites owned by government-owned NDA. Financing government support is Treasury, while the role of nuclear in levelling up is handled by Communities and Local Government. Suitability of international partners is assessed by the Foreign Office and national security implications through – for example – cyber-risk is Home Office.

With the promised establishment of Great British Nuclear (GBN), government has an opportunity (perhaps its last, if nuclear is to underpin its 2050 Net Zero target, as research shows it can) to catalyse the UK’s nuclear programme via a co-ordinated series of measures, accelerating delivery by picking a course and moving at pace, giving confidence to others to do likewise. This might be the only way to achieve a meaningful fleet of identical units (or multiple fleets, perhaps one for GW-scale plants and others for SMRs and AMRs), and thus bring the benefits – demonstrated elsewhere – from such series build, specifically reduced cost and timescales for developers and repeat business for the supply chain.

Nearer-term specific measures government could usefully take include:

- Establishing GBN with a suitable remit and the power to act across Whitehall, removing blockages and applying appropriate incentives.

- Financial support to encourage series reactor build – encouraging potential first movers, and incentivising subsequent investors to maximise the speed and effectiveness of delivery.

- Widening the scope of financial incentives, potentially on offer to communities which might host onshore wind, to include all low carbon generation – making community engagement a dialogue, not a plea to accept an unknown and largely unwanted technology.

Miss this chance, and the much-anticipated GBN simply becomes another talking shop developing options for endless government review. Then those investors and developers who might have invested in the UK will head abroad, and the opportunity is gone, leaving us with an energy landscape almost impossible to decarbonise.

Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

William Bodel is a Postdoctoral Research Associate at The University of Manchester’s Dalton Nuclear Institute. His previous work concerned life-extension of operating British reactors, and he is currently engaged in future reactor system choice.

How can nuclear help with energy costs - and how do we pay for nuclear?

William Bodel

Europe is struggling through a period of exorbitant energy prices. In addition to directly hitting consumers with a higher cost of living, high energy prices will also have detrimental effects on business and industry. In this blog, Will Bodel from the Dalton Nuclear Institute examines the role of nuclear energy in reducing the cost of energy, and discusses their funding and financing.

- New nuclear energy could provide a significant amount of Britain’s energy needs, which will help insulate against future energy shocks.

- Nuclear energy can be cost-effective, but requires a sensible approach to financing, which Government must facilitate.

- Progress has been made in developing a RAB financing model. The full details of the RAB are yet to be defined, but it is important to ensure that the operational costs are reasonable.

The current energy crisis

In August, Ofgem announced that the price cap (the backstop protection limiting the unit price suppliers could charge for energy), would rise to £3,549 for October-December 2022, a sharp increase from £1,250 last winter. With forecasters predicting prices would hit £4,500 in 2023, Government announced an Energy Price Guarantee, limiting the cap to a lower level to help protect consumers, with the taxpayer compensating energy suppliers the difference.

Government’s medium-term strategy remains to be seen, but it must involve starting to put in place a more resilient energy system to prevent recurrence. While new nuclear power can do little about the immediate problem, it has an important role in the long-term reshaping of the system and preventing such vulnerability in the future.

How could such a situation have been avoided?

One answer would have been a diversification of generation capacity; a broad portfolio of generation technology reduces vulnerability when one source becomes scarce. This is hardly a shocking revelation, and the use of energy supply as leverage is also nothing new – such a sentiment was expressed throughout the 2008 Energy White Paper:

“The majority of the UK’s nuclear power stations are due to close over the next two decades. Over the same period, the UK will become increasingly reliant on imports of oil and gas, and at a time of rising global demand and prices, and when energy supplies are becoming more politicised.”

Coal use had all but vanished in the UK as carbon reductions for net zero were pursued, and only five nuclear power plants remain operational (down from 16 in 2000). Meanwhile, the expansion of renewables proves a double-edged sword as gas is needed to fill in the gaps in their intermittency.

A role for nuclear?

Electricity from nuclear is low-carbon, not reliant on resources located in politically volatile regions, reliable, and cheap to fuel and maintain. Given all this, and if almost 15 years ago it was identified that new nuclear should be built, why is Hinkley Point C still the only nuclear plant under construction?

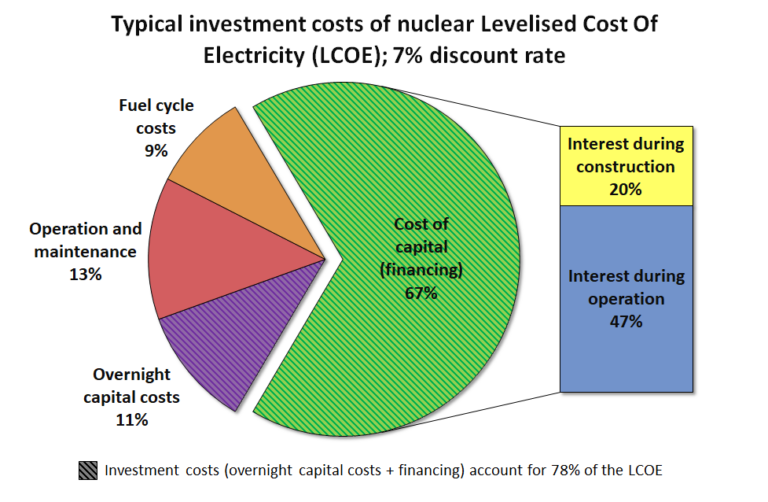

The reason is financing – a paradox exists on the economics of nuclear. Small marginal costs make nuclear power plants price competitive over their long (60+ year) lifetime, but this is only realised after the large initial capital costs are expended and the plant becomes operational. Long build times must be endured before any return on investment is seen, and it is during this long, high-risk construction period that financing costs balloon to dominate the total cost per unit of electricity (see Figure 1).

Figure 1. Breakdown of the nuclear levelised cost of electricity. Reproduced from NEA.

Figure 1. Breakdown of the nuclear levelised cost of electricity. Reproduced from NEA.

Financing options

Since Sizewell B (our most recent nuclear power plant) was built, state-financing nuclear power has been unpopular, and the huge capital costs and long repayment period has deterred private investment – alternative financing solutions have therefore been sought.

In 2012 the government committed to a Contract for Difference (CfD) for Hinkley Point C. This ensures that the operator EDF bears risk in delivering the project and funds eventual decommissioning, albeit with a government debt guarantee. Once built, the CfD guarantees EDF a minimum “strike price” of £89.50/MWh (inflation-linked, so £114 in today’s money) for 35 years after the project completion. At the time, with wholesale electricity prices just under £50/MWh, this was described by many as a bad deal for future bill payers, who are ultimately responsible for paying the strike price – but compared to today’s prices, the HPC strike price look rather better. That said, estimates from the Committee on Climate Change in 2013 predicted onshore wind costs in 2020 of £80/MWh and offshore wind £120/MWh, so the HPC strike price seemed not too bad a deal for reliable, low carbon electricity at the time.

A better deal may not have been possible using this financing method. While the strike price seems high by 2012 standards, the developer in a CfD shoulders the burden of constructing the plant – and the associated risk. Such an undertaking warrants such a strike price. The failure of other contemporary nuclear projects at Moorside and Wylfa (CfDs with lower strike prices) due to financing issues indicates how ineffective this method is for financing nuclear projects.

Alternative financing methods have been proposed, but the one identified as having the greatest potential is the Regulated Asset Base (RAB), the model used to fund Heathrow Terminal 5 and the Thames Tideway Tunnel. The RAB aims to make the whole process more affordable by empowering a regulator to levy charges on consumers while a plant is being built. While this means bill-payers will be paying for a plant which isn’t producing electricity yet, because project owners will be able to settle financing costs sooner in the life of the project (reducing the size of the green slice in Figure 1), this stops the financing costs from spiralling during the construction period. These savings can then be passed on to consumers in the form of cheaper electricity per unit, with figures of £40-£60/MWh being touted for electricity from future nuclear plants built according to this financing model.

The Nuclear Energy (Financing) Bill, introducing the RAB for nuclear received Royal Assent in March, but not all the details of how it will be operated have been decided. The latest step in the process, the Government’s consultation on the RAB revenue stream, closed in August and is currently being analysed. As the details are finalised it is important that the Government, and the relevant regulator, ensure the best possible deal for the consumer.

William Bodel is a Postdoctoral Research Associate at The University of Manchester’s Dalton Nuclear Institute. His previous work concerned life-extension of operating British reactors, and he is currently engaged in future reactor system choice.

How can “Great British Nuclear” make a great difference?

Adrian Bull

The announcement of Great British Nuclear (GBN) is a long awaited positive step. GBN clearly now faces a monumental workload and a range of challenges as it sets the ground for new nuclear build in the UK. In this article, Professor Adrian Bull emphasises the need to engage with development companies rather than just ‘starting from scratch’.

- Since the original plans for an SMR (Small Modular Reactor) competition in 2015, significant developments have been made.

- Less publicised have been the establishment of a number of development organisations which could prove to be vital in making new (small) nuclear a reality.

- Government should treat these development companies (DevCo’s) as clients for GBN who can act as the voice of regions and potentially of investors too.

Setting the ground for new nuclear build in the UK process starts with running a competition to find the best design of “Small Modular Reactor” (SMR). Although we may have been frustrated by the fact a similar-sounding SMR competition was launched back in 2015 by the then Chancellor George Osborne, we mustn’t fall into the trap of thinking there has been no progress since that time. In fact – many of the important cornerstones of today’s nuclear requirements have been delivered in the intervening years, and crucially to build on those, and not to work around them.

Groundwork and developments

A nuclear reactor development project – of any size – is about much more than the reactor itself. In addition to the choice of reactor design, a project needs funding, a market into which the electricity can be sold and regulatory approval (or at least a clear process via which such approvals can be obtained). But it also needs somewhere to go – in the form of a suitable site, as discussed in my recent article. And linked to the siting question, it needs a welcoming local community (or at least the absence of robust protest), with a skilled and available workforce for all parts of its planning, construction and operation.

Since the first plans for an SMR competition back in 2015, we’ve seen:

- The Nuclear Sector Deal in 2018 included provision for regulators to adapt their Generic Design Assessment (GDA) processes to be more flexible for the timely assessment of SMR designs.

- In April 2022, the RR SMR was the first such design to enter into a newly modernised, 3-step GDA process (adapted from the original 4-step model). And in January this year a further six reactor designs were submitted to the process.

- An Expert Finance Group was established and commissioned by Government to review financing of new nuclear in 2018. The work covered investment models, business structures and risk allocation – among other topics – and importantly concluded that there are alternatives to the traditional model of single organisation ownership which could be effective in delivering rollout of a significant SMR fleet. That is to say, investors and owners don’t have to be the utilities.

- A new Regulated Asset Base finance model for nuclear projects was introduced by Government in 2022.

Great British Nuclear – potential facilitators

The progress made has been well-publicised and welcomed by those in the industry. Though less well covered in the media was the establishment of a number of development organisations which could well prove to be vital in making new (small) nuclear a reality. These organisations – such as Solway Community Power in Cumbria and Cwmni Egino in North Wales – could well act as the catalysts for bringing the various pieces of the jigsaw together. Not only that – they can do so in a way which puts the local community and the site at the forefront of the project, rather than alienating key local stakeholders as some past projects have done.

These bodies can act as the mortar between the big “bricks” of regulation, reactor technology, financing and – crucially – government, to make sure that expectations are aligned, roles clear and sensitivities managed, especially in a local context with the multiple stakeholders on all sides. By working with them, understanding their position and listening to their needs, GBN can get a very good understanding of the landscape and what needs to be done most urgently.

It should be stressed – these development companies are not mere talking shops to shout from the side-lines or get in the way. They are led by senior figures with credibility and a track record of delivery. This credibility, and the respect they hold within a community, allows them to attract robust and reliable finance, without necessarily being long-established or having the deepest of pockets themselves.

Speeding up the process

They also have one massive advantage over Government – they can be far more agile. So they can go out to find the most suitable partners and strike arrangements without the lengthy process of consultation and “open to all” competition, both of which are good things – but not when pursued beyond reason. That means a more nimble and flexible approach to pulling teams together. Bringing in private finance in this way also helps to insulate any rollout of new nuclear from the pervasive treacle of Government spending review cycles. For the right project, a team can be brought together quickly by a DevCo and simply signed off by Government to help speed its progress.

As GBN is charged with “…driving delivery of new nuclear projects…”, inviting the DevCo’s to the table to update on their progress and to explain where they need help would be a great way to start. With a mammoth task to undertake from a standing start, GBN may well find that there are partially formed solutions already out there which simply need help and encouragement, without the need to go back to the drawing board. The DevCo’s can effectively become clients for GBN and can act as the voice of regions and potentially of investors too.

So when GBN launch their competition to deliver SMR technology to the UK, I urge them to avoid simply asking for all the reactor vendors to send in their glossy brochures and over-optimistic delivery timescales, and instead to ask “bring us your SMR-focused solutions, and tell us how we can make them happen”. That way, they can use the good work already done as a springboard to deliver progress, rather than simply starting from scratch.

Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

Analysis and ideas on going nuclear, curated by Policy@Manchester

At Manchester, our energy experts are committed to delivering an equitable and prosperous net zero energy future. By matching science and engineering, with social science, economics, politics and arts, the University’s community of 600+ experts address the entire lifecycle of each energy challenge, creating innovative and enduring solutions to make a difference to the lives of people around the globe. This enables the university's research community to develop pathways to ensure a low carbon energy transition that will also drive jobs, prosperity, resilience and equality.

Realising sustainable futures requires new and integrative solutions to address the interacting global environmental challenges.

Sustainable Futures brings together the unique depth and breadth of internationally leading research at The University of Manchester and builds on the University’s track record of successful interdisciplinary working, to produce integrated and truly sustainable solutions to urgent environmental challenges

With special thanks to our contributors:

Dr William Bodel is a Postdoctoral Research Associate at The University of Manchester’s Dalton Nuclear Institute. His previous work concerned life-extension of operating British reactors, and he is currently engaged in future reactor system choice.

Professor Gregg Butler is Head of Strategic Assessment for The University of Manchester’s Dalton Nuclear Institute. He has published extensively on a broad range of nuclear topics, and was a member of the Committee on Radioactive Waste Management from 2012 to 2019.

Professor Juan Matthews is Visiting Professor in Nuclear Energy Technology at The University of Manchester’s Dalton Nuclear Institute. With a career spanning over 50 years, he has experience in nuclear and high technology industries across Europe, Asia, Russia and the Americas, and was formerly the nuclear specialist at UK Trade and Investment (now Department of International Trade).

Professor Francis Livens is Professor of Radiochemistry. He has acted as an advisor to the nuclear industry both in the UK and overseas and holds a range of external roles, including Chair of the Nuclear Innovation and Research Advisory Board (NIRAB) and a member of the Nuclear Decommissioning Authority Board.

Professor Adrian Bull is BNFL chair in Nuclear Energy and Society at The University of Manchester’s Dalton Nuclear Institute. Until June 2022 he was also Director of External Relations for the UK National Nuclear Laboratory. He is closely involved with a wide range of stakeholders including politicians, Government officials, media, customers, industry organisations and universities, and was awarded an MBE for his work on improving stakeholder engagement around nuclear issues.

Dr Aneeqa Khan is a research fellow in Nuclear Fusion working at the University of Manchester at Harwell and in the Department of Engineering for Sustainability, School of Engineering.

All opinions and recommendations made by article authors are made on the basis of their research evidence and experience in their fields. Evidence and further discussion can be obtained by correspondence with the authors; please contact policy@manchester.ac.uk in the first instance.

Read more and join the debate at: blog.policy.manchester.ac.uk

www.policy.manchester.ac.uk

@UoMPolicy #GoingNuclear

December 2022

The University of Manchester

Oxford Road, Manchester

M13 9PL

United Kingdom

The opinions and views expressed in this publication are those of the respective authors and do not necessarily reflect the views of The University of Manchester.